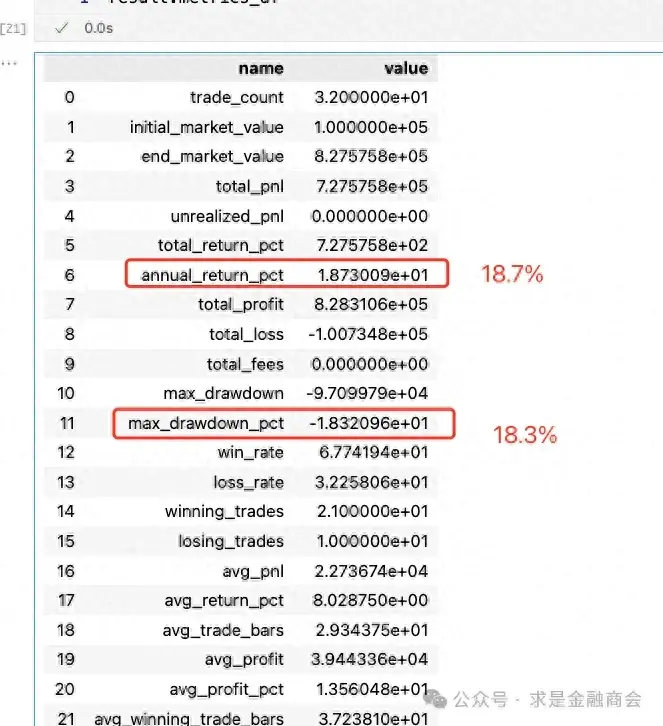

一.效果

二.实现

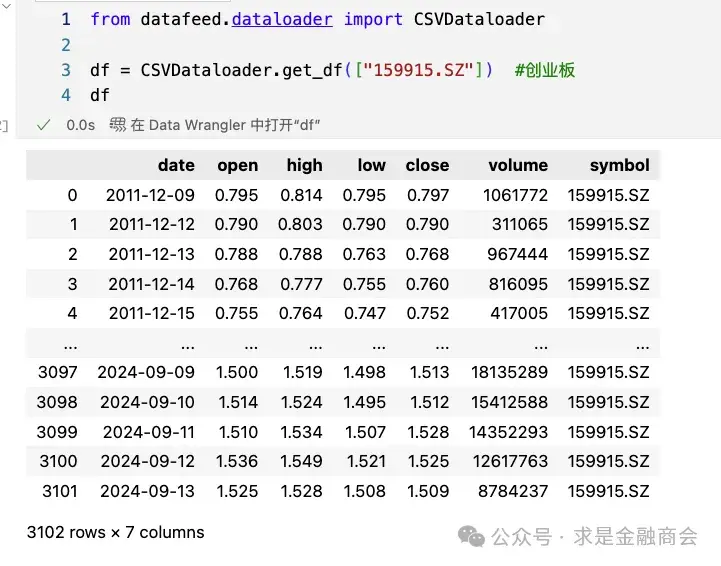

1.获取数据

2.用talib定义动量指标

#https://www.pybroker.com/zh-cn/latest/notebooks/5.%20Writing%20Indicators.html#%E4%BD%BF%E7%94%A8-TA-Lib

# rsi_20 = pybroker.indicator('rsi_20', lambda data: talib.RSI(data.close, timeperiod=20))

#talib 获取标的20日收益率数据,计算20日收益率

roc_20 = pybroker.indicator('roc_20', lambda data: talib.ROC(data.close, timeperiod=20)/100)

roc_20(df)3.定义买入卖出规则函数

#https://www.pybroker.com/zh-cn/latest/notebooks/2.%20Backtesting%20a%20Strategy.html#%E5%AE%9A%E4%B9%89%E7%AD%96%E7%95%A5%E8%A7%84%E5%88%99

#如果没有持仓,20日roc大于8%时买入100%

#如果20日roc小于0时,卖出所有

def pick_time(ctx):

if not ctx.long_pos() and ctx.indicator("roc_20")[-1] > 0.08:

ctx.buy_shares = ctx.calc_target_shares(1.0)

if ctx.indicator("roc_20")[-1] < 0:

ctx.sell_all_shares()4.回测

from pybroker import Strategy, StrategyConfig

config = StrategyConfig(bars_per_year=252, exit_on_last_bar=True)

#1.策略起始时间和结束时间

strategy = Strategy(df, "20111209", "20240913", config)

#2.对标的159915 添加pick_time 执行条件,用到了roc_20指标

strategy.add_execution(pick_time, ["159915.SZ"], indicators=[roc_20])

result = strategy.backtest()

发布者:股市刺客,转载请注明出处:https://www.95sca.cn/archives/268138

站内所有文章皆来自网络转载或读者投稿,请勿用于商业用途。如有侵权、不妥之处,请联系站长并出示版权证明以便删除。敬请谅解!