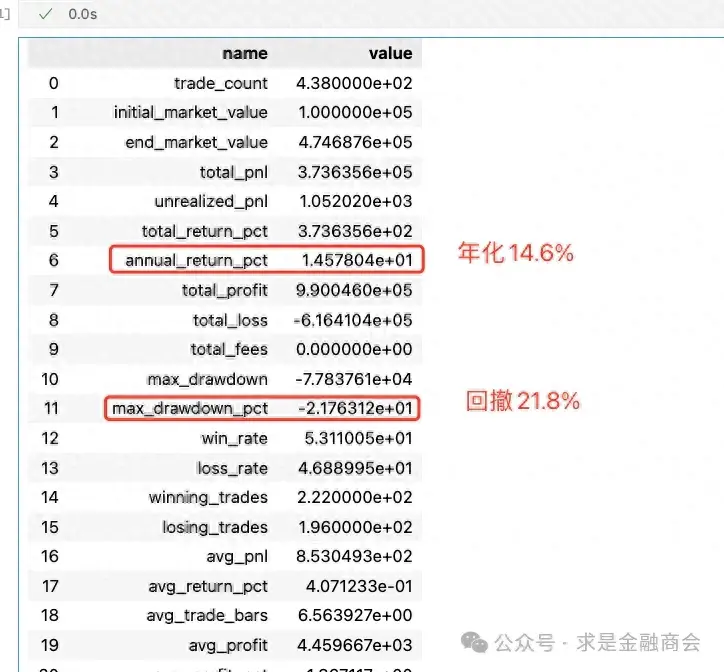

一.效果

二.实现

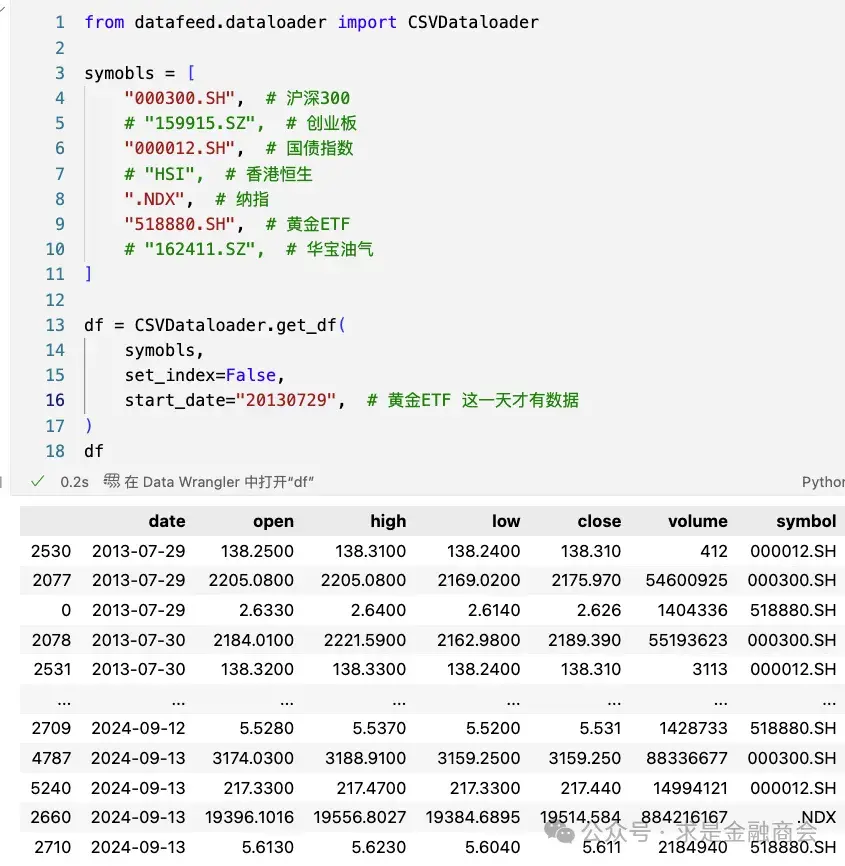

1.第一步获取df数据

2.获取动量指标数据

# https://www.pybroker.com/zh-cn/latest/notebooks/5.%20Writing%20Indicators.html#%E4%BD%BF%E7%94%A8-TA-Lib

# rsi_20 = pybroker.indicator('rsi_20', lambda data: talib.RSI(data.close, timeperiod=20))

# talib 获取标的20日收益率数据,计算20日收益率

roc_20 = pyb.indicator(

"roc_20", lambda data: talib.ROC(data.close, timeperiod=20) / 100

)3.设置交易规则,定义排序函数,轮转函数

# https://www.pybroker.com/zh-cn/latest/notebooks/10.%20Rotational%20Trading.html

# 购买 20 天涨幅(ROC)最高的buy_nums只股票。

# 将我们的资本的 1/buy_nums 分配给每只股票。

# 如果其中一只股票不再位于前buy_nums名的 20 天涨幅(ROC)中,则我们将清盘该股票。

# 每天交易这些规则。

buy_nums = 1

config = StrategyConfig(max_long_positions=buy_nums, bars_per_year=252, exit_on_last_bar=True)

pyb.param("target_size", 1 / config.max_long_positions)

pyb.param("rank_threshold", buy_nums) # 排名阀值

# 实现一个排名函数,根据每只股票的 20 天涨幅(ROC)降序 排列,从最高到最低。

def rank(ctxs: dict[str, ExecContext]):

scores = {symbol: ctx.indicator("roc_20")[-1] for symbol, ctx in ctxs.items()}

sorted_scores = sorted(

scores.items(), key=lambda score: score[1], reverse=True # 降序

)

threshold = pyb.param("rank_threshold")

top_scores = sorted_scores[:threshold]

top_symbols = [score[0] for score in top_scores]

pyb.param("top_symbols", top_symbols)

# 实现一个 轮动 函数来管理轮动交易。

def rotate(ctx: ExecContext):

if ctx.long_pos():

if ctx.symbol not in pyb.param("top_symbols"):

ctx.sell_all_shares()

else:

target_size = pyb.param("target_size")

ctx.buy_shares = ctx.calc_target_shares(target_size)

ctx.score = ctx.indicator("roc_20")[-1]4.执行回测

# 1.策略起始时间和结束时间

strategy = Strategy(df, "20130729", "20240913", config)

# 2.先排序

strategy.set_before_exec(rank)

# 3.执行轮转策略

strategy.add_execution(rotate, symobls, indicators=[roc_20])

result = strategy.backtest()

发布者:股市刺客,转载请注明出处:https://www.95sca.cn/archives/268137

站内所有文章皆来自网络转载或读者投稿,请勿用于商业用途。如有侵权、不妥之处,请联系站长并出示版权证明以便删除。敬请谅解!

![[通达信画线指标]缠论2源码 高低点连线 辅助看趋势 摆动高低点 数波浪 形态 1到3组参数可调](https://95sca.cn/2024/08/07/rTibmY9sMW9H6sw1722995202.0718644.jpg?imageMogr2/thumbnail/!480x300r|imageMogr2/gravity/center/crop/480x300)

![[通达信指标]一线判顶底公式代码含选股](https://95sca.cn/2024/08/07/TrzjduqMd1QrM1A1722998375.4973526.jpg?imageMogr2/thumbnail/!480x300r|imageMogr2/gravity/center/crop/480x300)

![[通达信指标]好指标 瀑布金牛王公式](https://95sca.cn/2024/08/07/AQTGwrjMVMDMjNw1722997118.322136.jpg?imageMogr2/thumbnail/!480x300r|imageMogr2/gravity/center/crop/480x300)