除了少数的投资策略,比如套利之外,多数投资组合的构建思路都可归为“多因子模型”。因子可以是基本面,技术面,另类数据等。

单个标的的操作,比如期货、BTC等,重要技术指标加上仓位策略。仓位策略,止盈损之类的非常关键。

而组合型的投资,如etf,转债,股票等,一般不会重仓单支,而是投资组合的形式,这里就涉及一个优先的问题,优选的本质就是“多因子模型”。当然也可以附加大盘择时。

多因子模型一般是轮动模型,就是定期评估组合内各标的的得分,持有得分高的,卖出得分低的。

轮动模型,核心是对某因子进行排序,选得分高的TOP K个。

轮动算子

class SelectTopK:

def __init__(self, K=1, order_by='order_by', b_ascending=False):

self.K = K

self.order_by = order_by

self.b_ascending = b_ascending

def __call__(self, ctxs: dict[str, ExecContext], *args, **kwargs):

selected = None

if pyb.param('selected'):

selected = pyb.param('selected')

scores = {}

for symbol, ctx in ctxs.items():

if selected and symbol not in selected:

continue scores[symbol] = ctx.indicator(self.order_by)[-1] sorted_scores = sorted( scores.items(), key=lambda score: score[1], reverse=True ) threshold = self.K top_scores = sorted_scores[:threshold] top_symbols = [score[0] for score in top_scores] pyb.param('selected', top_symbols)

规则选股

这里就是传统规则型多因子策略的逻辑,比如roc_20>0.08 且均线20突破收盘价,甚至可以加上3个条件满足2个及以上即可。

正则表达式加上eval,相当的强大!!!

class SelectBySignal: def __init__(self, buy_rules=[], buy_at_least_count=1, sell_rules=[], sell_rules_at_least_count=1): self.buy_rules = buy_rules self.buy_at_least_count = buy_at_least_count self.sell_rules = sell_rules self.sell_rules_at_least_count = sell_rules_at_least_count def _check_if_matched(self, ctxs, rules, at_least_count): matched_items = [] for symbol, ctx in ctxs.items(): match = 0 for i, rule in enumerate(rules): expr = re.sub('ind\((.*)\)', 'ctx.indicator("\\1")[-1]', rule) if eval(expr): match += 1 if match >= at_least_count: matched_items.append(symbol) return matched_items def __call__(self, ctxs): to_buy = self._check_if_matched(ctxs, self.buy_rules, self.buy_at_least_count) to_sell = self._check_if_matched(ctxs, self.sell_rules, self.sell_rules_at_least_count) holding = utils.get_current_holdings(ctxs) new_hold = list(set(to_buy + holding)) for s in to_sell: if s in new_hold: new_hold.remove(s) pyb.param('selected', new_hold)

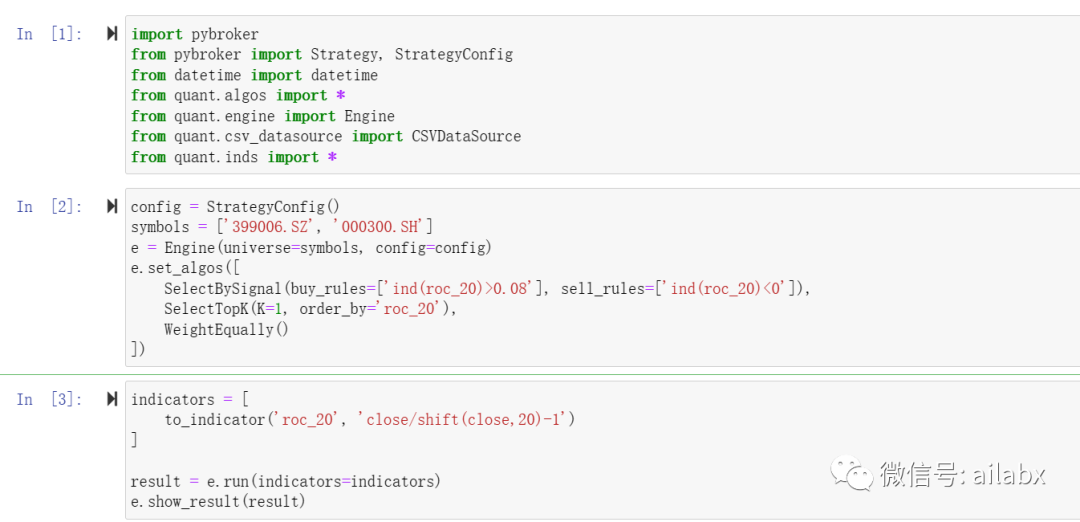

完成了以上模型,我们来写一个策略就非常简单了:

动量轮动及排序:

买入条件:20日动量>0.08,

卖出条件:20日动量<0。

排序条件:20日动量倒序,如果超过1支,则选择20日动量最大的那支持有。

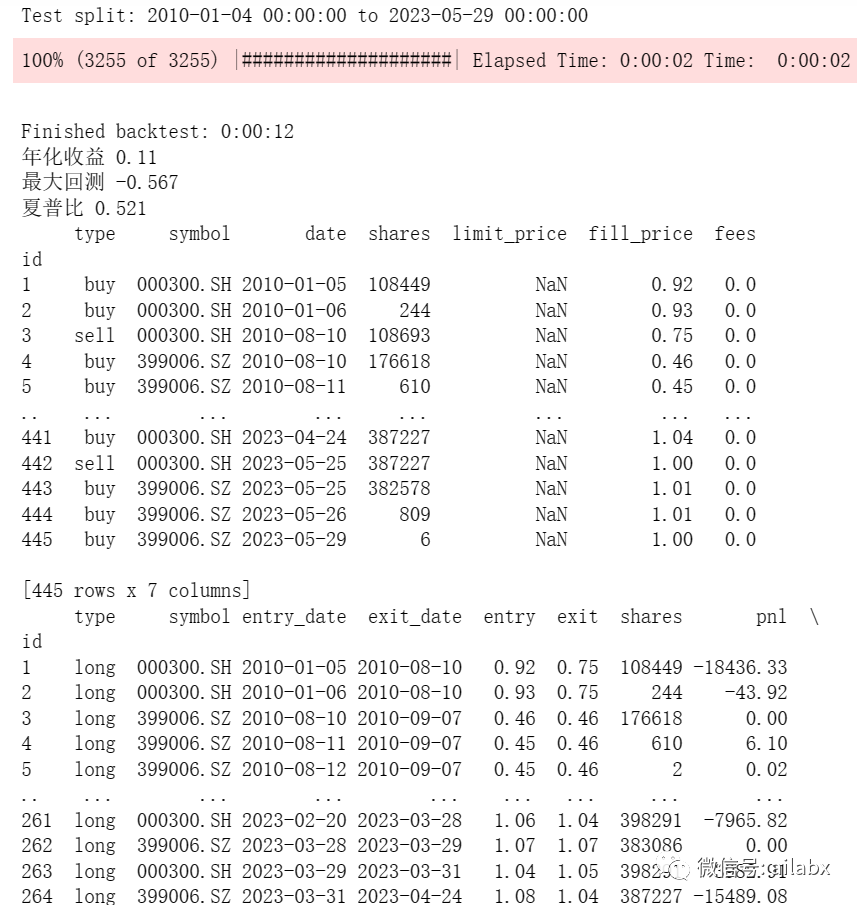

年化11%,回撤有点大,明天我们使用真实的ETF来轮动,同时加上RSRS的大盘择时。

今天的代码在(代码与数据均发布至星球,请前往下载):

ETF的列表,我们可以选择几十支有代表性的宽基、行业指数来动量轮动,后面考虑引入基本面、资金面,拥挤度等。

发布者:股市刺客,转载请注明出处:https://www.95sca.cn/archives/104123

站内所有文章皆来自网络转载或读者投稿,请勿用于商业用途。如有侵权、不妥之处,请联系站长并出示版权证明以便删除。敬请谅解!