一、引言

二、配对交易策略概述

三、策略构建步骤

-

交易对象选取:选择两个具有协整关系的资产。

-

数据收集:获取资产的历史价格数据。

-

协整检验:检验两个资产价格序列是否协整。

-

投资组合构建:基于协整关系构建投资组合。

-

设置阈值:确定开仓和止损的阈值。

-

历史回测:使用历史数据测试策略的有效性。

四、Python实现过程

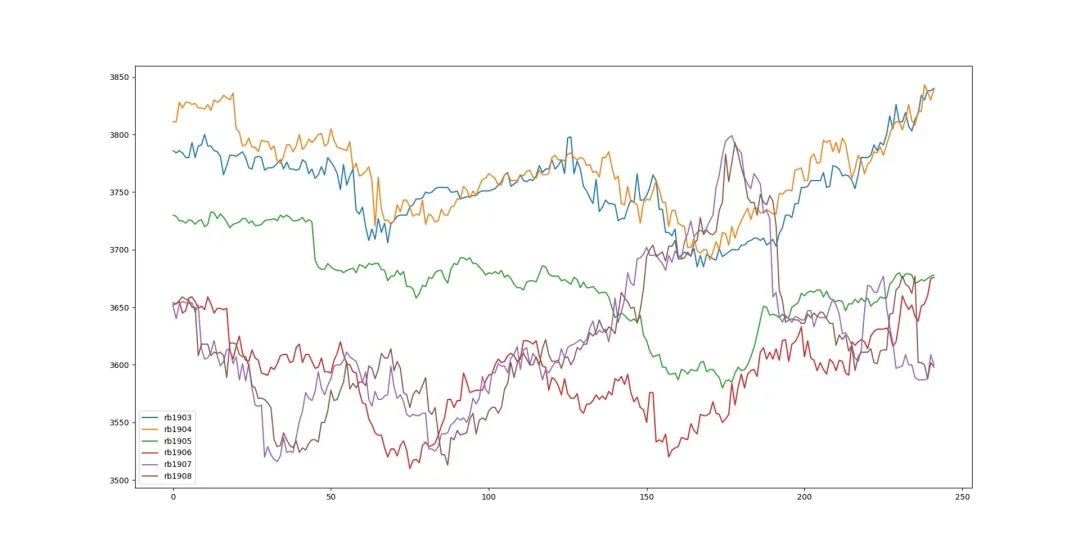

1. 数据收集

def fetch_data(ids): url_5m = 'http://stock2.finance.sina.com.cn/futures/api/json.php/IndexService.getInnerFuturesMiniKLine5m?symbol=' result = [] for id in ids: url = url_5m + id req = urllib2.Request(url) rsp = urllib2.urlopen(req) res = rsp.read() res_json = json.loads(res) result.append(res_json) close_result = [] for instrument in result: oneDay_list = [] for oneDay in instrument: oneDay_list.append(float(oneDay[-2])) close_result.append(np.array(oneDay_list)) close_result = np.array(close_result) close_result = close_result.T df = pd.DataFrame(data=close_result, columns=ids) return df2. 协整检验

from statsmodels.tsa.stattools import adfuller, coint

def check_stationarity(price): result = adfuller(price) print(result)

def check_coint(price_A, price_B): result = coint(price_A, price_B) print(result)3. 投资组合构建与阈值设置

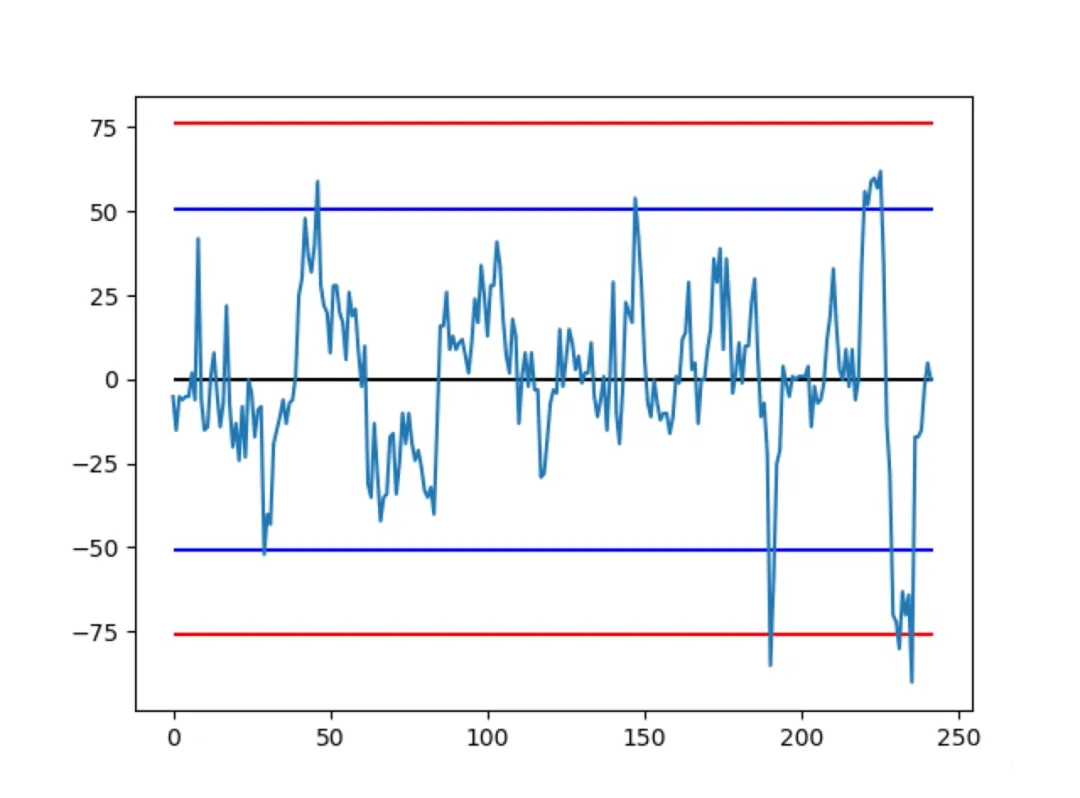

def strategy(df, sigma): price_A = df['rb1907'].values price_B = df['rb1908'].values spread = price_A - price_B mspread = spread - np.mean(spread) open_threshold = 2 * sigma stop_threshold = 3 * sigma

# Plotting the spread and thresholds fig = plt.figure() ax = fig.add_subplot(111) ax.plot(range(len(mspread)), mspread) ax.hlines(0, 0, len(mspread)) ax.hlines(open_threshold, 0, len(mspread), colors='b') ax.hlines(-stop_threshold, 0, len(mspread), colors='b') ax.hlines(stop_threshold, 0, len(mspread), colors='r') ax.hlines(-stop_threshold, 0, len(mspread), colors='r') plt.show()

4. 历史回测

def strategy(): df = pd.read_csv('./data.csv') price_A = df['rb1907'].values price_B = df['rb1908'].values spread = price_A - price_B mspread = spread - np.mean(spread) sigma = np.std(mspread) open = 2 * sigma stop = 3 * sigma profit_list = [] hold = False hold_price_A = 0 hold_price_B = 0 hold_state = 0 # 1 (A:long B:short) -1 (A:short B:long) profit_sum = 0 for i in range(len(price_A)): if hold == False: if mspread[i] >= open: hold_price_A = price_A[i] hold_price_B = price_B[i] hold_state = -1 hold = True elif mspread[i] <= -open: hold_price_A = price_A[i] hold_price_B = price_B[i] hold_state = 1 hold = True else: if mspread[i] >= stop and hold_state == -1: profit = (hold_price_A - price_A[i]) + (price_B[i] - hold_price_B) profit_sum += profit hold_state = 0 hold = False elif mspread[i] <= -stop and hold_state == 1: profit = (price_A[i] - hold_price_A) + (hold_price_B - price_B[i]) profit_sum += profit hold_state = 0 hold = False if mspread[i] <= 0 and hold_state == -1: profit = (hold_price_A - price_A[i]) + (price_B[i] - hold_price_B) profit_sum += profit hold_state = 0 hold = False if mspread[i] >= 0 and hold_state == 1: profit = (price_A[i] - hold_price_A) + (hold_price_B - price_B[i]) profit_sum += profit hold_state = 0 hold = False profit_list.append(profit_sum) print(profit_list) fig = plt.figure() ax = fig.add_subplot(111) profit_list) plt.show()结论

发布者:股市刺客,转载请注明出处:https://www.95sca.cn/archives/106042

站内所有文章皆来自网络转载或读者投稿,请勿用于商业用途。如有侵权、不妥之处,请联系站长并出示版权证明以便删除。敬请谅解!