开始之前,来句鸡汤提提神。

you got a dream,you gotta protect it,if you want something,go get it.如果你有梦想,就要守护它,如果你想要什么,就去实现它。

人的一生,没有标准答案,不违背公序良俗的前提下,按自己喜欢的方式过一生就是成功。

在模型方面,我们从随机森林开始,因为它很简单,然后过渡到lightGBM,xgboost,之前就是深度模型,主要基于pytorch(fastai),以及部分keras。

以决策树为基本学习单元的集成学习,对于表格型数据的处理,在kaggle这样的比赛中大放异彩。决策树的逻辑,与多因子很像。其余的模型,把因子都当成向量中的一个维度,决策树就是一个“因子”。比如择偶,身高>173吗?体重<150斤吗?年收入大于XX等等。在多因子选股中也类似,净利润增长是否为下,RSRS是否大于0.8?

随机森林说是把一堆决策树“打包(bagging)”在一起,共同决策。每次都是“随机”,“有放回”抽样,然后得到一个结果。

pip install scikit-learn即可。它依赖scipy,numpy。

传统机器学习sklearn基本够了。

深度学习我们以pytorch为主,我直接安装fastai,它依赖pytorch, pandas, spacy,依赖的包比较多。

另外keras会一并安装,一些量化的模型是使用keras来实现了。

pip install keras,keras本身支持tensorflow,cntk以及theano作为backend,所以并未强制安装tensorflow。

集成学习的特点:

- 它可以处理数千个输入变量而无需变量删除。

- 它给出了对分类中哪些变量重要的估计。

这两点非常重要,因子好与坏往上堆就是了,模型会自动筛选出来好的。

模型从使用上非常简单:

from sklearn.ensemble import RandomForestRegressor reg = RandomForestRegressor(random_state=20) reg.fit(X,y)

这里我需要准备数据,X,y,X就是多因子特征,y是label数据标注,一般我们选择“未来N天的”收益率。

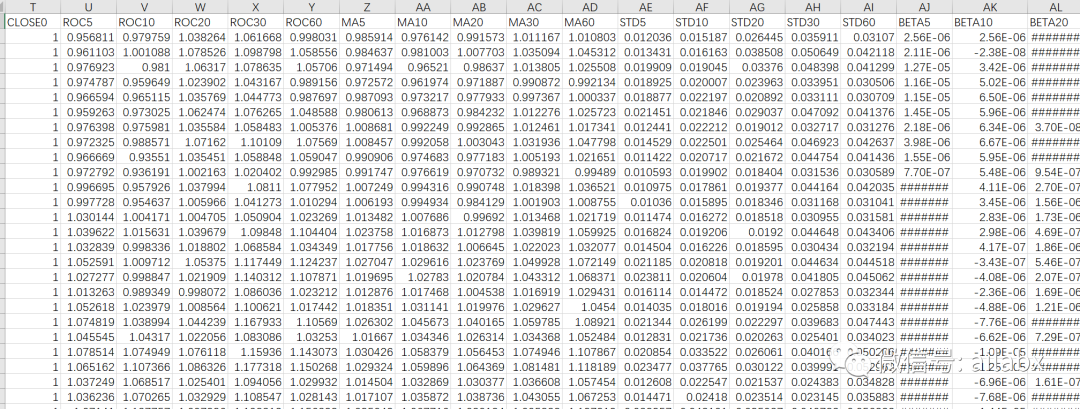

这里借用下qlib的alpha158的因子库,对全球指数进行158个因子的计算。

import pandas as pd class Alpha158_Dataset: def get_label_config(self): return ["Ref($close, -20)/Ref($close, -1) - 1"], ["LABEL0"] def get_feature_config(self): conf = { "kbar": {}, "price": { "windows": [0], "feature": ["OPEN", "HIGH", "LOW", "CLOSE"], }, "rolling": {}, } return self.parse_config_to_fields(conf) @staticmethod def parse_config_to_fields(config): """create factors from config config = { 'kbar': {}, # whether to use some hard-code kbar features 'price': { # whether to use raw price features 'windows': [0, 1, 2, 3, 4], # use price at n days ago 'feature': ['OPEN', 'HIGH', 'LOW'] # which price field to use }, 'volume': { # whether to use raw volume features 'windows': [0, 1, 2, 3, 4], # use volume at n days ago }, 'rolling': { # whether to use rolling operator based features 'windows': [5, 10, 20, 30, 60], # rolling windows size 'include': ['ROC', 'MA', 'STD'], # rolling operator to use #if include is None we will use default operators 'exclude': ['RANK'], # rolling operator not to use } } """ fields = [] names = [] if "kbar" in config: fields += [ "($close-$open)/$open", "($high-$low)/$open", "($close-$open)/($high-$low+1e-12)", "($high-Greater($open, $close))/$open", "($high-Greater($open, $close))/($high-$low+1e-12)", "(Less($open, $close)-$low)/$open", "(Less($open, $close)-$low)/($high-$low+1e-12)", "(2*$close-$high-$low)/$open", "(2*$close-$high-$low)/($high-$low+1e-12)", ] names += [ "KMID", "KLEN", "KMID2", "KUP", "KUP2", "KLOW", "KLOW2", "KSFT", "KSFT2", ] if "price" in config: windows = config["price"].get("windows", range(5)) feature = config["price"].get("feature", ["OPEN", "HIGH", "LOW", "CLOSE", "VWAP"]) for field in feature: field = field.lower() fields += ["Ref($%s, %d)/$close" % (field, d) if d != 0 else "$%s/$close" % field for d in windows] names += [field.upper() + str(d) for d in windows] if "volume" in config: windows = config["volume"].get("windows", range(5)) fields += ["Ref($volume, %d)/($volume+1e-12)" % d if d != 0 else "$volume/($volume+1e-12)" for d in windows] names += ["VOLUME" + str(d) for d in windows] if "rolling" in config: windows = config["rolling"].get("windows", [5, 10, 20, 30, 60]) include = config["rolling"].get("include", None) exclude = config["rolling"].get("exclude", []) # `exclude` in dataset config unnecessary filed # `include` in dataset config necessary field def use(x): return x not in exclude and (include is None or x in include) # Some factor ref: https://guorn.com/static/upload/file/3/134065454575605.pdf if use("ROC"): # https://www.investopedia.com/terms/r/rateofchange.asp # Rate of change, the price change in the past d days, divided by latest close price to remove unit fields += ["Ref($close, %d)/$close" % d for d in windows] names += ["ROC%d" % d for d in windows] if use("MA"): # https://www.investopedia.com/ask/answers/071414/whats-difference-between-moving-average-and-weighted-moving-average.asp # Simple Moving Average, the simple moving average in the past d days, divided by latest close price to remove unit fields += ["Mean($close, %d)/$close" % d for d in windows] names += ["MA%d" % d for d in windows] if use("STD"): # The standard diviation of close price for the past d days, divided by latest close price to remove unit fields += ["Std($close, %d)/$close" % d for d in windows] names += ["STD%d" % d for d in windows] if use("BETA"): # The rate of close price change in the past d days, divided by latest close price to remove unit # For example, price increase 10 dollar per day in the past d days, then Slope will be 10. fields += ["Slope($close, %d)/$close" % d for d in windows] names += ["BETA%d" % d for d in windows] if use("RSQR"): pass # The R-sqaure value of linear regression for the past d days, represent the trend linear #fields += ["Rsquare($close, %d)" % d for d in windows] #names += ["RSQR%d" % d for d in windows] if use("RESI"): pass # The redisdual for linear regression for the past d days, represent the trend linearity for past d days. #fields += ["Resi($close, %d)/$close" % d for d in windows] #names += ["RESI%d" % d for d in windows] if use("MAX"): # The max price for past d days, divided by latest close price to remove unit fields += ["Max($high, %d)/$close" % d for d in windows] names += ["MAX%d" % d for d in windows] if use("LOW"): # The low price for past d days, divided by latest close price to remove unit fields += ["Min($low, %d)/$close" % d for d in windows] names += ["MIN%d" % d for d in windows] if use("QTLU"): # The 80% quantile of past d day's close price, divided by latest close price to remove unit # Used with MIN and MAX fields += ["Quantile($close, %d, 0.8)/$close" % d for d in windows] names += ["QTLU%d" % d for d in windows] if use("QTLD"): # The 20% quantile of past d day's close price, divided by latest close price to remove unit fields += ["Quantile($close, %d, 0.2)/$close" % d for d in windows] names += ["QTLD%d" % d for d in windows] if use("RANK"): # Get the percentile of current close price in past d day's close price. # Represent the current price level comparing to past N days, add additional information to moving average. fields += ["Rank($close, %d)" % d for d in windows] names += ["RANK%d" % d for d in windows] if use("RSV"): # Represent the price position between upper and lower resistent price for past d days. fields += ["($close-Min($low, %d))/(Max($high, %d)-Min($low, %d)+1e-12)" % (d, d, d) for d in windows] names += ["RSV%d" % d for d in windows] if use("IMAX"): # The number of days between current date and previous highest price date. # Part of Aroon Indicator https://www.investopedia.com/terms/a/aroon.asp # The indicator measures the time between highs and the time between lows over a time period. # The idea is that strong uptrends will regularly see new highs, and strong downtrends will regularly see new lows. fields += ["IdxMax($high, %d)/%d" % (d, d) for d in windows] names += ["IMAX%d" % d for d in windows] if use("IMIN"): # The number of days between current date and previous lowest price date. # Part of Aroon Indicator https://www.investopedia.com/terms/a/aroon.asp # The indicator measures the time between highs and the time between lows over a time period. # The idea is that strong uptrends will regularly see new highs, and strong downtrends will regularly see new lows. fields += ["IdxMin($low, %d)/%d" % (d, d) for d in windows] names += ["IMIN%d" % d for d in windows] if use("IMXD"): # The time period between previous lowest-price date occur after highest price date. # Large value suggest downward momemtum. fields += ["(IdxMax($high, %d)-IdxMin($low, %d))/%d" % (d, d, d) for d in windows] names += ["IMXD%d" % d for d in windows] if use("CORR"): # The correlation between absolute close price and log scaled trading volume fields += ["Corr($close, Log($volume+1), %d)" % d for d in windows] names += ["CORR%d" % d for d in windows] if use("CORD"): # The correlation between price change ratio and volume change ratio fields += ["Corr($close/Ref($close,1), Log($volume/Ref($volume, 1)+1), %d)" % d for d in windows] names += ["CORD%d" % d for d in windows] if use("CNTP"): # The percentage of days in past d days that price go up. fields += ["Mean($close>Ref($close, 1), %d)" % d for d in windows] names += ["CNTP%d" % d for d in windows] if use("CNTN"): # The percentage of days in past d days that price go down. fields += ["Mean($close<Ref($close, 1), %d)" % d for d in windows] names += ["CNTN%d" % d for d in windows] if use("CNTD"): # The diff between past up day and past down day fields += ["Mean($close>Ref($close, 1), %d)-Mean($close<Ref($close, 1), %d)" % (d, d) for d in windows] names += ["CNTD%d" % d for d in windows] if use("SUMP"): # The total gain / the absolute total price changed # Similar to RSI indicator. https://www.investopedia.com/terms/r/rsi.asp fields += [ "Sum(Greater($close-Ref($close, 1), 0), %d)/(Sum(Abs($close-Ref($close, 1)), %d)+1e-12)" % (d, d) for d in windows ] names += ["SUMP%d" % d for d in windows] if use("SUMN"): # The total lose / the absolute total price changed # Can be derived from SUMP by SUMN = 1 - SUMP # Similar to RSI indicator. https://www.investopedia.com/terms/r/rsi.asp fields += [ "Sum(Greater(Ref($close, 1)-$close, 0), %d)/(Sum(Abs($close-Ref($close, 1)), %d)+1e-12)" % (d, d) for d in windows ] names += ["SUMN%d" % d for d in windows] if use("SUMD"): # The diff ratio between total gain and total lose # Similar to RSI indicator. https://www.investopedia.com/terms/r/rsi.asp fields += [ "(Sum(Greater($close-Ref($close, 1), 0), %d)-Sum(Greater(Ref($close, 1)-$close, 0), %d))" "/(Sum(Abs($close-Ref($close, 1)), %d)+1e-12)" % (d, d, d) for d in windows ] names += ["SUMD%d" % d for d in windows] if use("VMA"): # Simple Volume Moving average: https://www.barchart.com/education/technical-indicators/volume_moving_average fields += ["Mean($volume, %d)/($volume+1e-12)" % d for d in windows] names += ["VMA%d" % d for d in windows] if use("VSTD"): # The standard deviation for volume in past d days. fields += ["Std($volume, %d)/($volume+1e-12)" % d for d in windows] names += ["VSTD%d" % d for d in windows] if use("WVMA"): # The volume weighted price change volatility fields += [ "Std(Abs($close/Ref($close, 1)-1)*$volume, %d)/(Mean(Abs($close/Ref($close, 1)-1)*$volume, %d)+1e-12)" % (d, d) for d in windows ] names += ["WVMA%d" % d for d in windows] if use("VSUMP"): # The total volume increase / the absolute total volume changed fields += [ "Sum(Greater($volume-Ref($volume, 1), 0), %d)/(Sum(Abs($volume-Ref($volume, 1)), %d)+1e-12)" % (d, d) for d in windows ] names += ["VSUMP%d" % d for d in windows] if use("VSUMN"): # The total volume increase / the absolute total volume changed # Can be derived from VSUMP by VSUMN = 1 - VSUMP fields += [ "Sum(Greater(Ref($volume, 1)-$volume, 0), %d)/(Sum(Abs($volume-Ref($volume, 1)), %d)+1e-12)" % (d, d) for d in windows ] names += ["VSUMN%d" % d for d in windows] if use("VSUMD"): # The diff ratio between total volume increase and total volume decrease # RSI indicator for volume fields += [ "(Sum(Greater($volume-Ref($volume, 1), 0), %d)-Sum(Greater(Ref($volume, 1)-$volume, 0), %d))" "/(Sum(Abs($volume-Ref($volume, 1)), %d)+1e-12)" % (d, d, d) for d in windows ] names += ["VSUMD%d" % d for d in windows] return fields, names def get_all_fields_names(self): fields, names = self.get_feature_config() fields_label, names_label = self.get_label_config() fields += fields_label names += names_label return fields, names, if __name__ == '__main__': fields, names = Alpha158_Dataset().get_all_fields_names() from quant_project.dataloader.dataloader import Dataloader df = Dataloader().load_datas('__all__', names=names, fields=fields) df.to_csv('features.csv') with pd.HDFStore('features.h5')as s: s['alpha158'] = df

然后保存到csv和hdf5里备用,这里都是价量数据。

csv的因子数据68M,h5格式的33M。

我们的label是预测“未来20天的收益率”,我们是按月度调仓,所以这个20天比较合理。

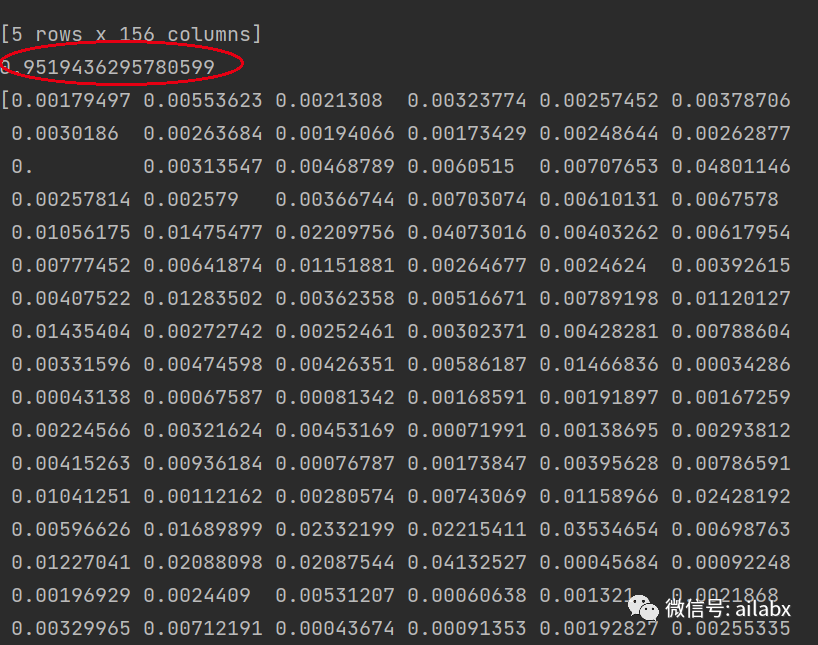

拟合得分95.1%,下面是各个维度的得分。

但是测试集上是负分!明显过拟合了。

发布者:股市刺客,转载请注明出处:https://www.95sca.cn/archives/104156

站内所有文章皆来自网络转载或读者投稿,请勿用于商业用途。如有侵权、不妥之处,请联系站长并出示版权证明以便删除。敬请谅解!